[55]:

import matplotlib as mpl

import matplotlib.pyplot as plt

from matplotlib.ticker import MaxNLocator, FormatStrFormatter

import numpy as np

import TransportMaps as TM

import TransportMaps.Maps as MAPS

import TransportMaps.Distributions as DIST

import TransportMaps.Diagnostics as DIAG

from TransportMaps import KL

mpl.rcParams['font.size'] = 15

Sequential inference via low-dimensional couplings¶

We use here the stochastic volatility model to present the decomposability of transports when the target density \(\nu_\pi\) is a Markov field. The following model is described in [OR7] and [OR8]. The transport map treatment of the problem is described in the paper [TM4] whose results are reported [here].

We model the log-volatility \({\bf Z}_{\Lambda}\) of the return of a financial asset at times \(\Lambda=\{0,1,\ldots,n\}\) with the autoregressive process

For \(k \in \Xi \subset \Lambda\), estimate parameters \(\Theta = (\mu,\phi)\) and states \(\left\{ {\bf Z}_k \right\}\), given observations

We want to characterize

where

Let us import the module for decomposable distributions …

[2]:

import TransportMaps.Distributions.Decomposable as DECDIST

… and a module with the definition of the building blocks of this problem …

[3]:

import TransportMaps.Distributions.Examples.StochasticVolatility as SV

… let us define \(\pi\left(\Theta\right)\) …

[4]:

is_mu_h = True

is_sigma_h = False

is_phi_h = True

pi_hyper = SV.PriorHyperParameters(is_mu_h, is_sigma_h, is_phi_h, 1)

… the initial density \(\pi\left(\left.{\bf Z}_{0} \right\vert \Theta\right)\) and transition densities \(\pi\left(\left.{\bf Z}_{k} \right\vert {\bf Z}_{k-1}, \Theta\right)\) …

[5]:

mu_h = SV.IdentityFunction()

phi_h = SV.F_phi(3.,1.)

sigma_h = SV.ConstantFunction(0.25)

pi_ic = SV.PriorDynamicsInitialConditions(

is_mu_h, mu_h, is_sigma_h, sigma_h, is_phi_h, phi_h)

pi_trans = SV.PriorDynamicsTransition(

is_mu_h, mu_h, is_sigma_h, sigma_h, is_phi_h, phi_h)

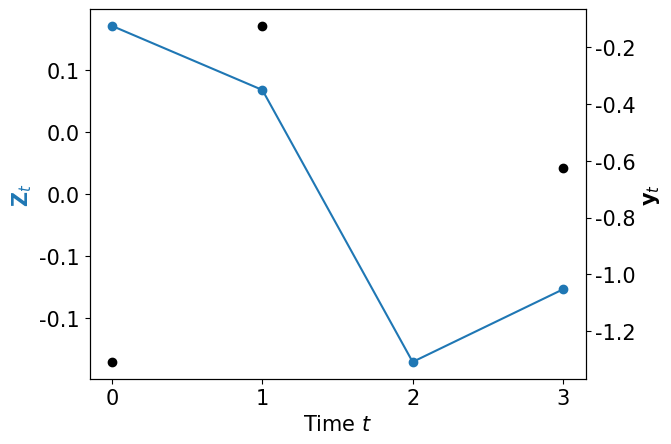

Now it’s time to generate some data \({\bf y}_\Xi\) (missing observation 2) …

[6]:

def plot_data_dynamics(Zt, yt, fig=None):

if fig is None:

fig = plt.figure()

ax1 = fig.add_subplot(111)

ax2 = ax1.twinx()

l1, = ax1.plot(Zt, 'o-')

ax1.set_xlabel(r"Time $t$")

ax1.set_ylabel(r"${\bf Z}_t$")

ax2.plot(yt, 'ko')

ax2.set_ylabel(r"${\bf y}_t$")

ax1.xaxis.set_major_locator(MaxNLocator(integer=True))

ax1.yaxis.set_major_formatter(FormatStrFormatter('%.1f'))

ax2.yaxis.set_major_formatter(FormatStrFormatter('%.1f'))

ax1.yaxis.label.set_color(l1.get_color())

[7]:

mu = -.5

phi = .95

sigma = 0.25

nsteps = 4

yB, ZA = SV.generate_data(nsteps, mu, sigma, phi)

yB[2] = None # Missing data y2

plot_data_dynamics(ZA, yB)

Let’s then define \(\pi\left( \left. \Theta, {\bf Z}_\Lambda \right\vert {\bf y}_\Xi \right)\) where we sequentially assimilate \({\bf y}_\Xi\) …

[8]:

pi = DECDIST.HiddenMarkovChainDistribution(

pi_markov=DECDIST.MarkovChainDistribution([], pi_hyper),

ll_list=[]

)

for n, yt in enumerate(yB):

if yt is None:

ll = None

else:

ll = SV.LogLikelihood(yt, is_mu_h, is_sigma_h, is_phi_h)

if n == 0: pin = pi_ic

else: pin = pi_trans

pi.append(pin, ll)

… check how non-Gaussian is \(\pi\left( \left. \Theta, {\bf Z}_\Lambda \right\vert {\bf y}_\Xi \right)\) using its Laplace approximation \(\widetilde{\pi}\) …

[9]:

lap = TM.laplace_approximation(pi)

2023-03-26 00:36:16 WARNING: TransportMaps: laplace_approximation(): Sampling from the prior is not implemented. Initial conditions set to zero.

… and computing the diagnostic \(\mathbb{V}{\rm ar}_{\widetilde{\pi}}\left( \log \frac{\widetilde{\pi}}{\pi} \right)\)

[10]:

var = DIAG.variance_approx_kl(lap, pi, qtype=0, qparams=10000)

print("Variance diagnostic: %e" % var)

Variance diagnostic: 1.370653e+00

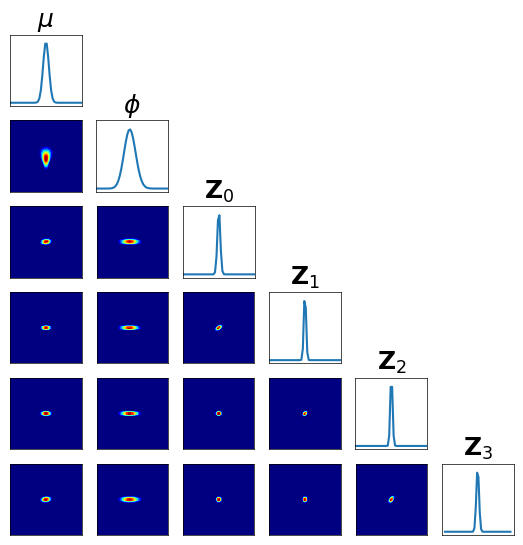

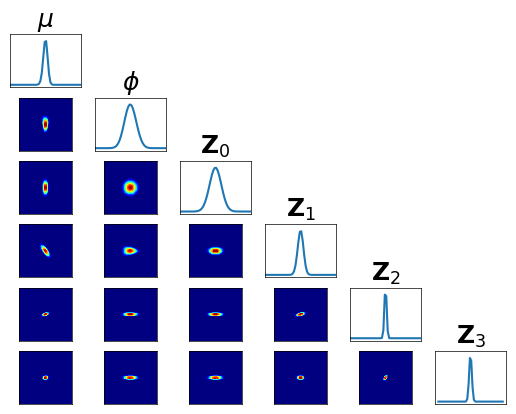

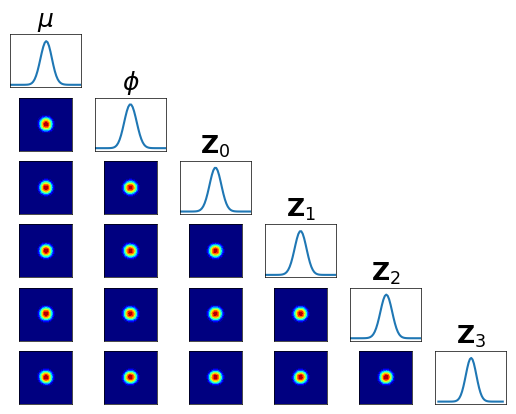

… We can also visualize the conditionals of \(\pi\left( \left. \Theta, {\bf Z}_\Lambda \right\vert {\bf y}_\Xi \right)\) …

[11]:

fig = plt.figure(figsize=(6.5,6.5))

fig = DIAG.plotAlignedConditionals( pi, range_vec=[-6,6],

numPointsXax=50, fig=fig, show_flag=False,

vartitles=[r"$\mu$",r"$\phi$",r"${\bf Z}_0$",r"${\bf Z}_1$",r"${\bf Z}_2$",r"${\bf Z}_3$"])

The direct approximation of \(\pi\left( \left. \Theta, {\bf Z}_\Lambda \right\vert {\bf y}_\Xi \right)\) is impractical:

It may be high-dimensional depending on the number of time steps

We may want to be able to update the approximation as we assimilate data

Low-dimensional couplings¶

We start with finding the map

that pushes forward \(\mathcal{N}(0,{\bf I})\) to the first Markov component of \(\pi\left( \left. \Theta, {\bf Z}_\Lambda \right\vert {\bf y}_\Xi \right)\):

Define the map \(R_0\), the permutation map \(Q\) and the Markov component \(\pi^0\) …

[12]:

order = 3

Q = MAPS.PermutationTransportMap([0,1,3,2])

R0 = MAPS.assemble_IsotropicIntegratedSquaredTriangularTransportMap(

dim=4, order=order)

pi0 = pi.get_MarkovComponent(-1)

Let us then setup and solve the problem

[13]:

rho = DIST.StandardNormalDistribution(dim=4)

pull_Q_pi0 = DIST.PullBackTransportMapDistribution(Q, pi0)

push_R0_rho = DIST.PushForwardTransportMapDistribution(R0, rho)

pull_R0_Q_pi0 = DIST.PullBackParametricTransportMapDistribution(R0, pull_Q_pi0)

qtype = 3 # Gauss quadrature

qparams = [6]*4 # Quadrature order

tol = 1e-4 # Optimization tolerance

ders = 2 # Use gradient and Hessian

log = KL.minimize_kl_divergence(

rho, pull_R0_Q_pi0, qtype=qtype, qparams=qparams,

tol=tol, ders=ders)

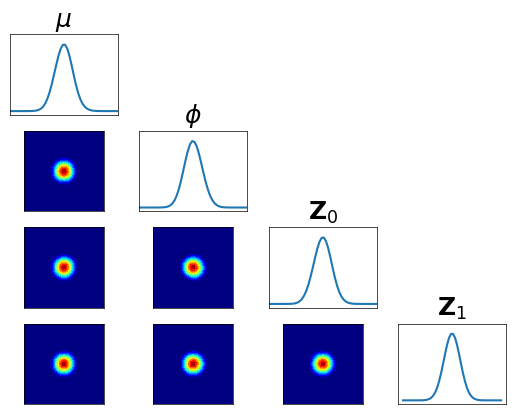

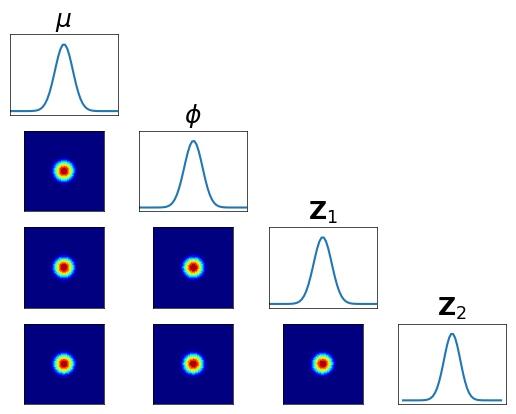

… check accuracy looking at conditionals of \(R_0^\sharp Q^\sharp \pi^0 \approx \rho\) …

[14]:

fig = plt.figure(figsize=(5.5,5.5))

varstr = [r"$\mu$",r"$\phi$",r"${\bf Z}_0$",r"${\bf Z}_1$"]

<Figure size 550x550 with 0 Axes>

[15]:

pull_R0_Q_pi0 = DIST.PullBackTransportMapDistribution(R0, pull_Q_pi0)

fig = DIAG.plotAlignedConditionals(pull_R0_Q_pi0, range_vec=[-6,6],

numPointsXax=50, fig=fig, show_flag=False, vartitles=varstr)

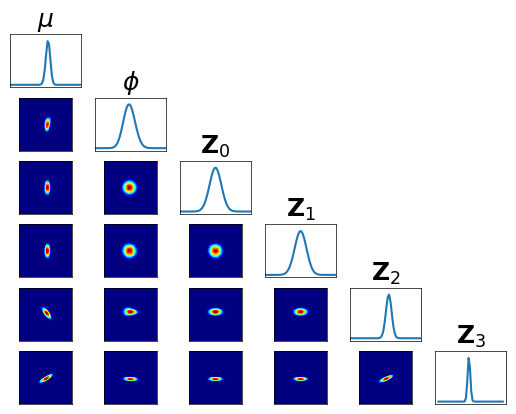

Let now \(T_0\) be

then for \({\bf X} \sim T_0^\sharp \pi\) we have \(\left.{\bf X}_0 {\perp\!\!\!\perp} {\bf X}_{i} \right\vert {\bf X}_{\{\theta,\Lambda\} \setminus \{0,i\}} \;\), for \(i\neq 0\).

Let us check the conditional independence of \(T_0^\sharp \pi\) …

[16]:

fig = plt.figure(figsize=(6,6))

varstr_all = [r"$\mu$",r"$\phi$",r"${\bf Z}_0$",r"${\bf Z}_1$",r"${\bf Z}_2$",r"${\bf Z}_3$"]

<Figure size 600x600 with 0 Axes>

[17]:

import TransportMaps.Maps.Decomposable as DECMAPS

M0 = MAPS.ListCompositeTransportMap(map_list=[Q, R0, Q])

Id = MAPS.IdentityTransportMap(M0.dim)

T0 = DECMAPS.SequentialMarkovChainTransportMap([M0,Id,Id], hyper_dim=2)

pull_T0_pi = DIST.PullBackTransportMapDistribution(T0, pi)

fig = DIAG.plotAlignedConditionals(pull_T0_pi, range_vec=[-6,6],

numPointsXax=50, fig=fig, show_flag=False, vartitles=varstr_all)

Let us now find the map

that pushes forward \(\mathcal{N}(0,{\bf I})\) to the second Markov component of \(T_0^\sharp \pi\):

[21]:

R1 = MAPS.assemble_IsotropicIntegratedSquaredTriangularTransportMap(

dim=4, order=order)

M0Theta = MAPS.ComponentwiseMap(active_vars=R0.active_vars[:2], approx_list=R0.approx_list[:2])

M01 = MAPS.ComponentwiseMap(active_vars=R0.active_vars[2:3], approx_list=R0.approx_list[2:3])

pi1 = pi.get_MarkovComponent(0, state_map=M01, hyper_map=M0Theta)

Let us then setup and solve the problem

[22]:

pull_Q_pi1 = DIST.PullBackTransportMapDistribution(Q, pi1)

pull_R1_Q_pi1 = DIST.PullBackParametricTransportMapDistribution(R1, pull_Q_pi1)

log = KL.minimize_kl_divergence(

rho, pull_R1_Q_pi1, qtype=qtype, qparams=qparams,

tol=tol, ders=ders)

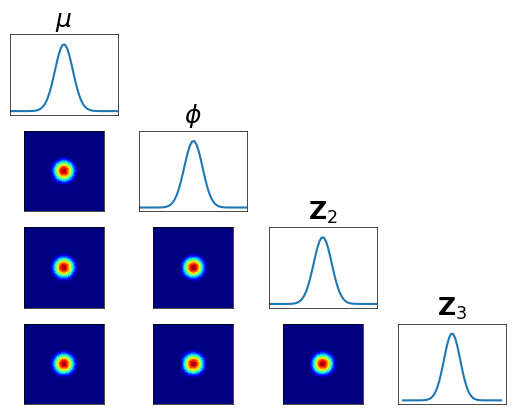

… check the accuracy looking at the conditionals of \(R_1^\sharp Q^\sharp \pi^1 \approx \rho\) …

[23]:

fig = plt.figure(figsize=(5.5,5.5))

varstr = [r"$\mu$",r"$\phi$",r"${\bf Z}_1$",r"${\bf Z}_2$"]

<Figure size 550x550 with 0 Axes>

[24]:

pull_R1_Q_pi1 = DIST.PullBackTransportMapDistribution(R1, pull_Q_pi1)

fig = DIAG.plotAlignedConditionals(pull_R1_Q_pi1, range_vec=[-6,6],

numPointsXax=50, fig=fig, show_flag=False, vartitles=varstr)

Let now \(T_1\) be

then for \({\bf X} \sim T_1^\sharp T_0^\sharp \pi\) we have \(\left.{\bf X}_{\{0,1\}} {\perp\!\!\!\perp} {\bf X}_{i} \right\vert {\bf X}_{\{\theta,\Lambda\} \setminus \{0,1,i\}} \;\), for \(i \notin \{0,1\}\).

Let us check the conditional independence of \(T_1^\sharp T_0^\sharp \pi\) …

[25]:

fig = plt.figure(figsize=(6,6))

<Figure size 600x600 with 0 Axes>

[26]:

M1 = MAPS.ListCompositeTransportMap(map_list=[Q, R1, Q])

T1T0 = DECMAPS.SequentialMarkovChainTransportMap([M0,M1,Id], hyper_dim=2)

pull_T1T0_pi = DIST.PullBackTransportMapDistribution(T1T0, pi)

fig = DIAG.plotAlignedConditionals(pull_T1T0_pi, range_vec=[-6,6],

numPointsXax=50, fig=fig, show_flag=False, vartitles=varstr_all)

Let us finally find the map

that pushes forward \(\mathcal{N}(0,{\bf I})\) to the third Markov component of \(T_1^\sharp T_0^\sharp \pi\):

[29]:

R2 = MAPS.assemble_IsotropicIntegratedSquaredTriangularTransportMap(

dim=4, order=order)

M1Theta = MAPS.ComponentwiseMap(active_vars=R1.active_vars[:2], approx_list=R1.approx_list[:2])

M0M1Theta = MAPS.CompositeMap(M0Theta, M1Theta)

M11 = MAPS.ComponentwiseMap(active_vars=R1.active_vars[2:3], approx_list=R1.approx_list[2:3])

pi2 = pi.get_MarkovComponent(1, state_map=M11, hyper_map=M0M1Theta)

Let us then setup and solve the problem

[30]:

pull_Q_pi2 = DIST.PullBackTransportMapDistribution(Q, pi2)

pull_R2_Q_pi2 = DIST.PullBackParametricTransportMapDistribution(R2, pull_Q_pi2)

log = KL.minimize_kl_divergence(

rho, pull_R2_Q_pi2, qtype=qtype, qparams=qparams,

tol=tol, ders=ders)

… check the accuracy looking at the conditionals of \(R_2^\sharp Q^\sharp \pi^2 \approx \rho\) …

[31]:

plt.figure(figsize=(5.5,5.5))

varstr = [r"$\mu$",r"$\phi$",r"${\bf Z}_2$",r"${\bf Z}_3$"]

<Figure size 550x550 with 0 Axes>

[32]:

pull_R2_Q_pi2 = DIST.PullBackTransportMapDistribution(R2, pull_Q_pi2)

fig = DIAG.plotAlignedConditionals(pull_R2_Q_pi2, range_vec=[-6,6],

numPointsXax=50, fig=fig, show_flag=False, vartitles=varstr)

Let now \(T_2\) be

then \(\mathfrak{T}^\sharp \pi := T_2^\sharp T_1^\sharp T_0^\sharp \pi \approx \mathcal{N}(0,{\bf I})\).

Let us check the conditional independence of \(\mathfrak{T}^\sharp \pi\) …

[33]:

fig = plt.figure(figsize=(6,6))

<Figure size 600x600 with 0 Axes>

[35]:

M2 = MAPS.ListCompositeTransportMap(map_list=[Q, R2, Q])

T = DECMAPS.SequentialMarkovChainTransportMap([M0,M1,M2], hyper_dim=2)

pull_T_pi = DIST.PullBackTransportMapDistribution(T, pi)

fig = DIAG.plotAlignedConditionals(pull_T_pi, range_vec=[-6,6],

numPointsXax=50, fig=fig, show_flag=False, vartitles=varstr_all)

… and we can compare its the variance \(\mathbb{V}{\rm ar}\left[ \frac{\rho}{\mathfrak{T}^\sharp \pi} \right]\) with the Laplace approximation …

[36]:

rho = DIST.StandardNormalDistribution(pull_T_pi.dim)

var_lap = DIAG.variance_approx_kl(lap, pi, qtype=0, qparams=10000)

var_seq = DIAG.variance_approx_kl(rho, pull_T_pi, qtype=0, qparams=10000)

print("Variance diagnostic - Laplace: %e" % var_lap)

print("Variance diagnostic - Sequential: %e" % var_seq)

Variance diagnostic - Laplace: 1.162491e+00

Variance diagnostic - Sequential: 8.439695e-02

Smoothing distribution¶

We can easily generate a biased sample of \(\pi\) via \(\mathfrak{T}_\sharp \rho \approx \pi\) …

[37]:

push_T_rho = DIST.PushForwardTransportMapDistribution(T, rho)

bias_samp_pi = push_T_rho.rvs(10000)

… or one can generate an unbiased Monte-Carlo Markov chain for \(\pi\) as follows:

generate a Markov chain (MC) with

invariant distribution \(T^\sharp \pi\)

using proposal distribution \(\rho\)

push forward the MC through T obtaining a MC with

invariant distribution \(\pi\).

[38]:

import TransportMaps.Samplers as SAMP

sampler = SAMP.MetropolisHastingsIndependentProposalsSampler(

pull_T_pi, rho)

burnin = 1000

(x, _) = sampler.rvs(10000)

x = x[burnin:,:]

unbias_samp_pi = T.evaluate(x) # Markov chain from \pi

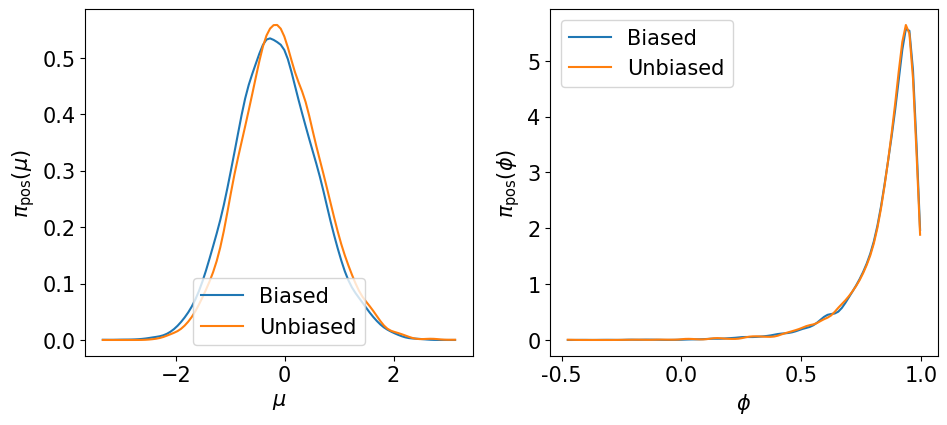

Let us visualize the marginals of the hyper-parameters \(\pi\left(\mu\left\vert {\bf y}_\Xi\right.\right)\) and \(\pi\left(\phi\left\vert {\bf y}_\Xi\right.\right)\) …

[39]:

def plot_marginal_hyper(bias_samp, unbias_samp):

import numpy as np

import scipy.stats as stats

fig = plt.figure(figsize=(11,4.5))

# \mu

ax1 = fig.add_subplot(121)

mu_bias_kde = stats.gaussian_kde(bias_samp[:,0])

mu_unbias_kde = stats.gaussian_kde(unbias_samp[:,0])

mu_min = min(np.min(bias_samp[:,0]), np.min(unbias_samp[:,0]))

mu_max = max(np.max(bias_samp[:,0]), np.max(unbias_samp[:,0]))

mu_x = np.linspace(mu_min, mu_max, 100)

ax1.plot(mu_x, mu_bias_kde(mu_x), label='Biased')

ax1.plot(mu_x, mu_unbias_kde(mu_x), label='Unbiased')

ax1.legend(loc='lower center')

ax1.set_xlabel(r"$\mu$")

ax1.set_ylabel(r"$\pi_{\rm pos}(\mu)$")

# \phi

ax2 = fig.add_subplot(122)

phi_bias_samp = phi_h.evaluate(bias_samp[:,1])

phi_unbias_samp = phi_h.evaluate(unbias_samp[:,1])

phi_bias_kde = stats.gaussian_kde(phi_bias_samp)

phi_unbias_kde = stats.gaussian_kde(phi_unbias_samp)

phi_min = min(np.min(phi_bias_samp), np.min(phi_unbias_samp))

phi_max = max(np.max(phi_bias_samp), np.max(phi_unbias_samp))

phi_x = np.linspace(phi_min, phi_max, 100)

ax2.plot(phi_x, phi_bias_kde(phi_x), label='Biased')

ax2.plot(phi_x, phi_unbias_kde(phi_x), label='Unbiased')

ax2.legend(loc='upper left')

ax2.set_xlabel(r"$\phi$")

ax2.set_ylabel(r"$\pi_{\rm pos}(\phi)$")

ax2.xaxis.set_major_formatter(FormatStrFormatter('%.1f'))

[40]:

plot_marginal_hyper(bias_samp_pi, unbias_samp_pi)

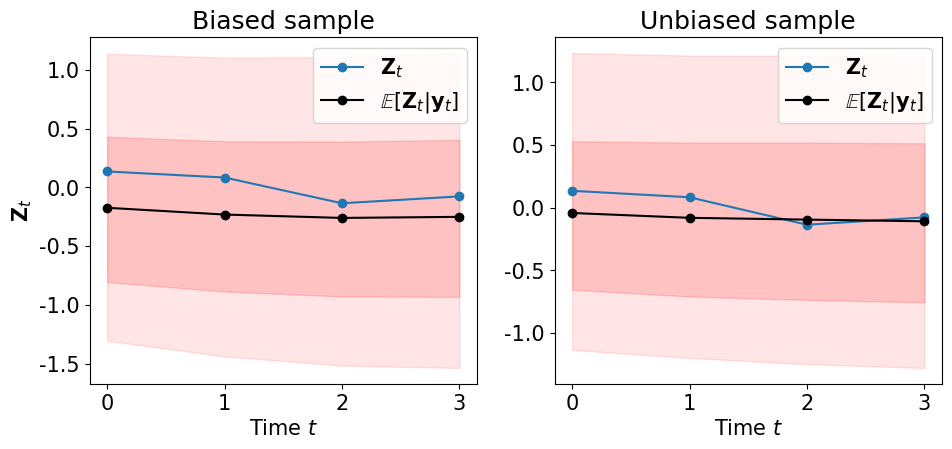

… the smoothing marginals of the states \(\pi\left(\left.{\bf Z}_k\right\vert {\bf y}_\Xi\right)\) …

[41]:

def plot_state_mean_percentiles(Zt, bias_samp, unbias_samp=None, fig=None, marker='o-'):

import numpy as np

if fig is None:

fig = plt.figure(figsize=(11,4.5))

# Biased

ax1 = fig.add_subplot(121)

l1, = ax1.plot(Zt, marker, label=r"${\bf Z}_t$")

ax1.set_xlabel(r"Time $t$")

ax1.set_ylabel(r"${\bf Z}_t$")

ax1.xaxis.set_major_locator(MaxNLocator(integer=True))

ax1.yaxis.set_major_formatter(FormatStrFormatter('%.1f'))

bias_mean = np.mean(bias_samp, axis=0)

bias_p5 = np.percentile(bias_samp, q=5., axis=0)

bias_p20 = np.percentile(bias_samp, q=20., axis=0)

bias_p80 = np.percentile(bias_samp, q=80., axis=0)

bias_p95 = np.percentile(bias_samp, q=95., axis=0)

ax1.plot(bias_mean, marker + 'k', label=r"$\mathbb{E}[{\bf Z}_t \vert {\bf y}_t]$")

ax1.fill_between(range(nsteps),y1=bias_p5, y2=bias_p95, color='r', alpha=.10)

ax1.fill_between(range(nsteps),y1=bias_p20, y2=bias_p80, color='r', alpha=.15)

ax1.legend()

ax1.set_title("Biased sample")

if unbias_samp is not None:

# Unbiased

ax2 = fig.add_subplot(122)

l1, = ax2.plot(Zt, marker, label=r"${\bf Z}_t$")

ax2.set_xlabel(r"Time $t$")

ax2.xaxis.set_major_locator(MaxNLocator(integer=True))

ax2.yaxis.set_major_formatter(FormatStrFormatter('%.1f'))

unbias_mean = np.mean(unbias_samp, axis=0)

unbias_p5 = np.percentile(unbias_samp, q=5., axis=0)

unbias_p20 = np.percentile(unbias_samp, q=20., axis=0)

unbias_p80 = np.percentile(unbias_samp, q=80., axis=0)

unbias_p95 = np.percentile(unbias_samp, q=95., axis=0)

ax2.plot(unbias_mean, marker+'k', label=r"$\mathbb{E}[{\bf Z}_t \vert {\bf y}_t]$")

ax2.fill_between(range(nsteps),y1=unbias_p5, y2=unbias_p95, color='r', alpha=.10)

ax2.fill_between(range(nsteps),y1=unbias_p20, y2=unbias_p80, color='r', alpha=.15)

ax2.legend()

ax2.set_title("Unbiased sample")

[42]:

plot_state_mean_percentiles(ZA, bias_samp_pi[:,2:], unbias_samp_pi[:,2:])

Filtering distribution¶

We have that

pushes forward \(\mathcal{N}(0,{\bf I})\) to the filtering distribution \(\pi\left(\left.\Theta,{\bf Z}_{k+1}\right\vert {\bf y}_{0:k+1} \right)\).

Let us generate samples for the filtering of the states \(\pi\left(\left.{\bf Z}_{k+1}\right\vert {\bf y}_{0:k+1} \right)\):

[43]:

R_list = [R0, R1, R2]

M1k_list = [

MAPS.ComponentwiseMap(

active_vars=R.active_vars[2:3],

approx_list=R.approx_list[2:3]

)

for R in R_list

]

filt_samp = np.zeros((10000,nsteps))

rho_0 = DIST.StandardNormalDistribution(4)

push = DIST.PushForwardTransportMapDistribution(M0, rho_0)

filt_samp[:,0:2] = push.rvs(10000)[:,2:4]

rho_filt = DIST.StandardNormalDistribution(3)

for n in range(2,nsteps):

filt_samp[:,n:n+1] = M1k_list[n-1].evaluate(rho_filt.rvs(10000))

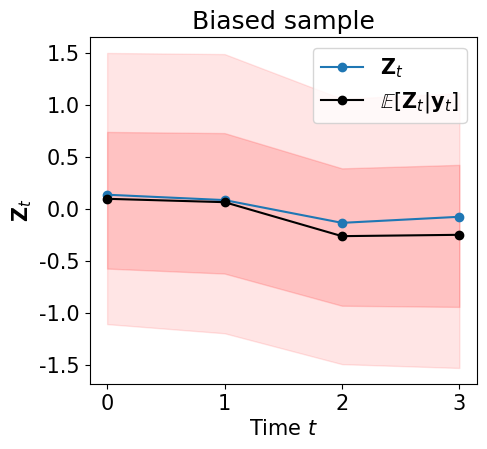

… and let us visualize \(\pi\left(\left.{\bf Z}_{k+1}\right\vert {\bf y}_{0:k+1} \right)\) …

[44]:

plot_state_mean_percentiles(ZA, filt_samp)

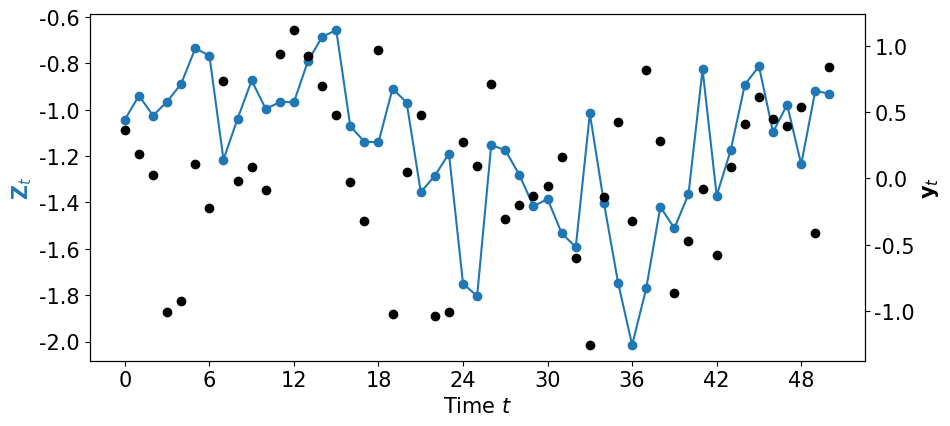

On-line data assimilation¶

Let us generate more data …

[45]:

nsteps = 51

yB, ZA = SV.generate_data(nsteps, mu, sigma, phi)

plot_data_dynamics(ZA, yB, fig=plt.figure(figsize=(10,4.5)))

… and let us assimilate these data on-line …

[56]:

import TransportMaps.Algorithms.SequentialInference as ALG

INT = ALG.TransportMapsSmoother(pi_hyper)

for n, yt in enumerate(yB):

if yt is None: ll = None # Missing data

else: ll = SV.LogLikelihood(yt, is_mu_h, is_sigma_h, is_phi_h)

if n == 0: pin = pi_ic # Prior initial conditions

else: pin = pi_trans # Prior transition dynamics

# Transport map specification

if n == 0: dim_tm = 3

else: dim_tm = 4

tm = MAPS.assemble_IsotropicIntegratedSquaredTriangularTransportMap(

dim=dim_tm, order=3)

# Solution parameters

solve_params = {'qtype': 3, 'qparams': [6]*dim_tm,

'tol': 1e-4}

# Regression map specification

hyper_tm = MAPS.assemble_IsotropicIntegratedSquaredTriangularTransportMap(

dim=pi_hyper.dim, order=4)

# Regression parameters

rho_hyper = DIST.StandardNormalDistribution(pi_hyper.dim)

reg_params = {'d': rho_hyper, 'qtype': 3, 'qparams': [7]*pi_hyper.dim,

'tol': 1e-4}

# Assimilation

print("%3d" % n, end="")

INT.assimilate(

pin, ll, tm, solve_params,

hyper_tm=hyper_tm, regression_params=reg_params)

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50

INT.assimilate takes care of approximating the map \(R_k\) using the transport map tm and the solution parameters solve_params (see TransportMap.minimize_kl_divergence). It also construct the map \(\mathfrak{M}_k = Q \circ R_k \circ Q\) and embeds it into the identity map \(T_k\).This allows a faster evaluation of the \(k\)-th Markov component, which depends on \(\mathfrak{H}_{k-1}\).

Let us check the accuracy using the diagnostic \(\mathbb{V}{\rm ar}\left[ \frac{\rho}{\mathfrak{T}^\sharp \pi} \right]\) …

[57]:

T = INT.smoothing_map

pi = INT.pi

pull_T_pi = DIST.PullBackTransportMapDistribution(T, pi)

rho = DIST.StandardNormalDistribution(pi.dim)

lap = TM.laplace_approximation(pi)

var_lap = DIAG.variance_approx_kl(lap, pi, qtype=0, qparams=10000)

var_seq = DIAG.variance_approx_kl(rho, pull_T_pi, qtype=0, qparams=10000)

print("Variance diagnostic - Laplace: %e" % var_lap)

print("Variance diagnostic - Sequential: %e" % var_seq)

2023-03-26 00:55:01 WARNING: TransportMaps: laplace_approximation(): Sampling from the prior is not implemented. Initial conditions set to zero.

Variance diagnostic - Laplace: 3.596890e+01

Variance diagnostic - Sequential: 1.654149e+00

Let us generate samples from \(\mathfrak{T}_\sharp \rho\) (biased samples of \(\pi\)) …

[58]:

push_T_rho = DIST.PushForwardTransportMapDistribution(T, rho)

bias_samp_pi = push_T_rho.rvs(10000)

… and unbiased samples from \(\pi\) …

[59]:

import TransportMaps.Samplers as SAMP

sampler = SAMP.MetropolisHastingsIndependentProposalsSampler(

pull_T_pi, rho)

(x, _) = sampler.rvs(10000)

x = x[5000:,:]

unbias_samp_pi = T.evaluate(x) # Markov chain from \pi

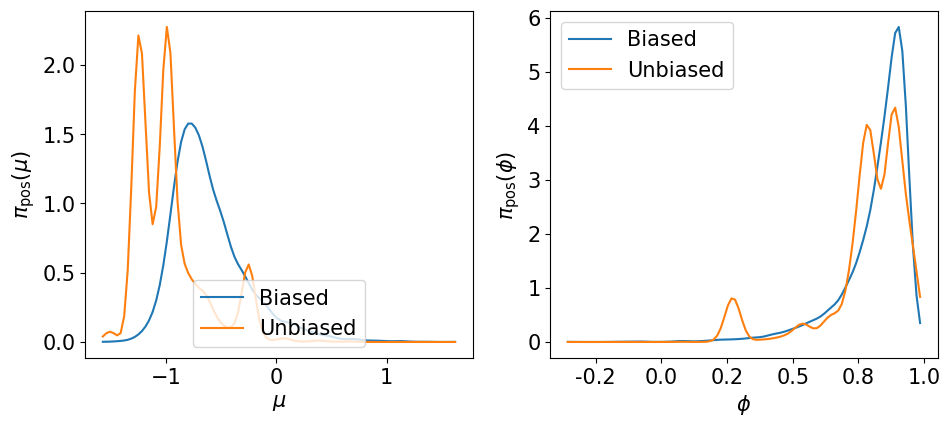

Let us visualize the marginals of the hyper-parameters \(\pi\left(\mu\left\vert {\bf y}_\Xi\right.\right)\) and \(\pi\left(\phi\left\vert {\bf y}_\Xi\right.\right)\) …

[60]:

plot_marginal_hyper(bias_samp_pi, unbias_samp_pi)

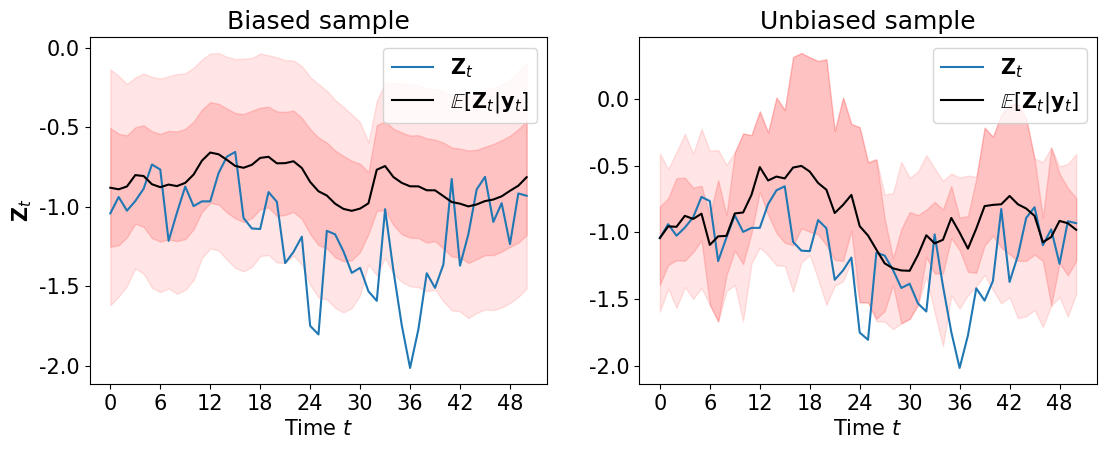

… and the smoothing marginals of the states \(\pi\left(\left.{\bf Z}_k\right\vert {\bf y}_\Xi\right)\) …

[61]:

plot_state_mean_percentiles(ZA, bias_samp_pi[:,2:], unbias_samp_pi[:,2:],

fig=plt.figure(figsize=(13,4.5)), marker='-')

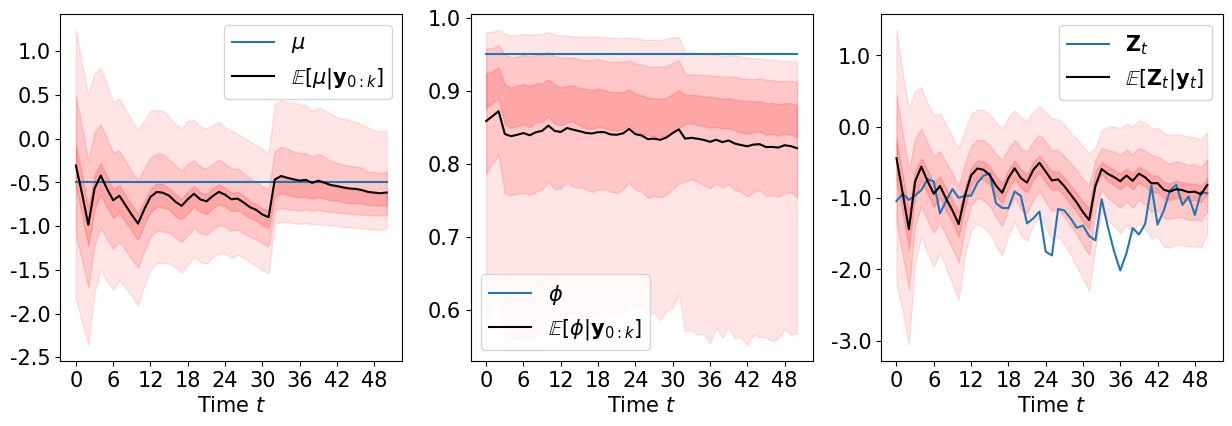

We can sample the filtering distributions \(\pi\left(\mu \middle\vert {\bf y}_{0:k}\right)\), \(\pi\left(\phi\middle\vert {\bf y}_{0:k}\right)\), \(\pi\left({\bf Z}_k\middle\vert {\bf y}_{0:k}\right)\) …

[62]:

filt_tm_list = INT.filtering_map_list

rho = DIST.StandardNormalDistribution(3)

samp_list = []

for tm in filt_tm_list:

push_tm_rho = DIST.PushForwardTransportMapDistribution(tm, rho)

samp_list.append( push_tm_rho.rvs(10000) )

… and visualize them …

[63]:

def plot_filtering(Zt, mu, phi, samp_list, fig=None, marker='o-'):

import numpy as np

mu_samp = np.vstack([ s[:,0] for s in samp_list ]).T

phi_samp = np.vstack([ s[:,1] for s in samp_list ]).T

phi_samp = phi_h.evaluate(phi_samp)

state_samp = np.vstack([ s[:,2] for s in samp_list ]).T

if fig is None:

fig = plt.figure(figsize=(15,4.5))

# mu

ax1 = fig.add_subplot(131)

ax1.plot(range(nsteps), np.ones(nsteps)*mu, marker, label=r"$\mu$")

ax1.set_xlabel(r"Time $t$")

#ax1.set_ylabel(r"$\mu$")

ax1.xaxis.set_major_locator(MaxNLocator(integer=True))

ax1.yaxis.set_major_formatter(FormatStrFormatter('%.1f'))

mean = np.mean(mu_samp, axis=0)

p5 = np.percentile(mu_samp, q=5., axis=0)

p20 = np.percentile(mu_samp, q=20., axis=0)

p40 = np.percentile(mu_samp, q=40., axis=0)

p60 = np.percentile(mu_samp, q=60., axis=0)

p80 = np.percentile(mu_samp, q=80., axis=0)

p95 = np.percentile(mu_samp, q=95., axis=0)

ax1.plot(mean, marker + 'k', label=r"$\mathbb{E}[\mu \vert {\bf y}_{0:k}]$")

ax1.fill_between(range(nsteps),y1=p5, y2=p95, color='r', alpha=.10)

ax1.fill_between(range(nsteps),y1=p20, y2=p80, color='r', alpha=.13)

ax1.fill_between(range(nsteps),y1=p40, y2=p60, color='r', alpha=.16)

ax1.legend()

# phi

ax2 = fig.add_subplot(132)

ax2.plot(range(nsteps), np.ones(nsteps)*phi, marker, label=r"$\phi$")

ax2.set_xlabel(r"Time $t$")

#ax2.set_ylabel(r"$\phi$")

ax2.xaxis.set_major_locator(MaxNLocator(integer=True))

ax2.yaxis.set_major_formatter(FormatStrFormatter('%.1f'))

mean = np.mean(phi_samp, axis=0)

p5 = np.percentile(phi_samp, q=5., axis=0)

p20 = np.percentile(phi_samp, q=20., axis=0)

p40 = np.percentile(phi_samp, q=40., axis=0)

p60 = np.percentile(phi_samp, q=60., axis=0)

p80 = np.percentile(phi_samp, q=80., axis=0)

p95 = np.percentile(phi_samp, q=95., axis=0)

ax2.plot(mean, marker + 'k', label=r"$\mathbb{E}[\phi \vert {\bf y}_{0:k}]$")

ax2.fill_between(range(nsteps),y1=p5, y2=p95, color='r', alpha=.10)

ax2.fill_between(range(nsteps),y1=p20, y2=p80, color='r', alpha=.13)

ax2.fill_between(range(nsteps),y1=p40, y2=p60, color='r', alpha=.16)

ax2.legend()

# states

ax3 = fig.add_subplot(133)

l1, = ax3.plot(Zt, marker, label=r"${\bf Z}_t$")

ax3.set_xlabel(r"Time $t$")

#ax3.set_ylabel(r"${\bf Z}_t$")

ax3.xaxis.set_major_locator(MaxNLocator(integer=True))

ax3.yaxis.set_major_formatter(FormatStrFormatter('%.1f'))

mean = np.mean(state_samp, axis=0)

p5 = np.percentile(state_samp, q=5., axis=0)

p20 = np.percentile(state_samp, q=20., axis=0)

p40 = np.percentile(state_samp, q=40., axis=0)

p60 = np.percentile(state_samp, q=60., axis=0)

p80 = np.percentile(state_samp, q=80., axis=0)

p95 = np.percentile(state_samp, q=95., axis=0)

ax3.plot(mean, marker + 'k', label=r"$\mathbb{E}[{\bf Z}_t \vert {\bf y}_t]$")

ax3.fill_between(range(nsteps),y1=p5, y2=p95, color='r', alpha=.10)

ax3.fill_between(range(nsteps),y1=p20, y2=p80, color='r', alpha=.13)

ax3.fill_between(range(nsteps),y1=p40, y2=p60, color='r', alpha=.16)

ax3.legend()

[64]:

plot_filtering(ZA, mu, phi, samp_list, marker='-')